Business

Onalaska state rep. Doyle will wait before pushing new PRAT legislation

Fueled by a huge voter approval at the polls this week, the ability of La Crosse County to get state approval for a new, special sales tax might have new energy.

Onalaska state rep. Steve Doyle says he won’t rush to reintroduce the so-called Premier Resort Area Tax. (PRAT). Not until it’s more clear what new government in Madison might provide counties for road funding in a new state budget.

“If we think we can get it a different way, that’s certainly better, if the state steps up and meets its obligation,” Doyle said.

County voters last Tuesday approved an advisory referendum on the PRAT by a more than two to one margin. It was the second successful advisory referendum for the measure.

The PRAT is a half-percent sales tax on most good sold in La Crosse County.

Doyle says he’s not opposed to reintroducing state legislation in Madison but there’s no rush for a couple reasons.

“I probably won’t push it,” Doyle said, “and there wouldn’t be any reason to push it until we find out what the budget looks like because really, we don’t pass bills that have financial impacts until after the budget.

“It’s something that will be out there for people to talk about but it’s really not going to be moving quickly just because of the nature of the process in Madison.”

Here’s the 16-page document on what the PRAT is and covers, exactly. Below is a list of of businesses it would affect.

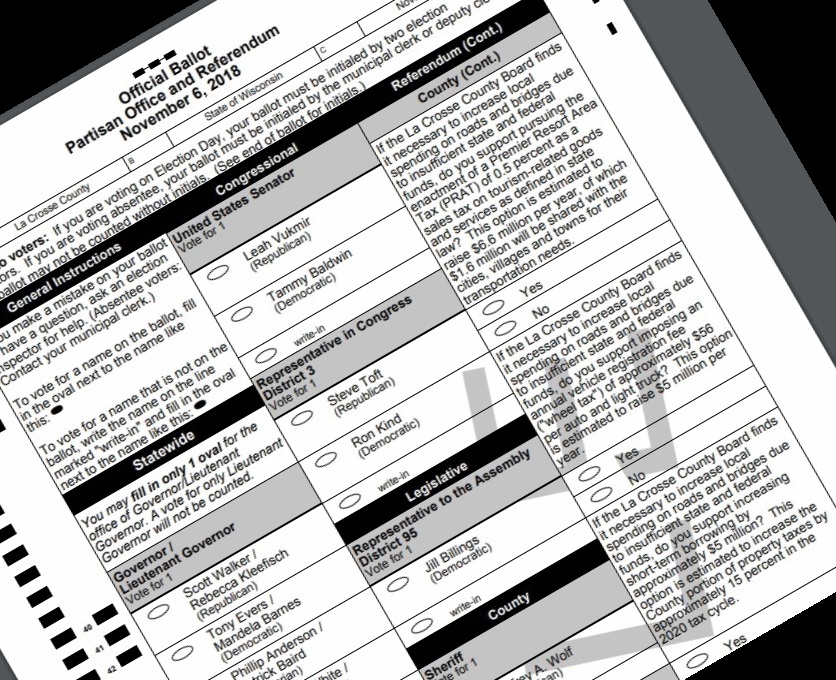

Here’s how it was worded on the ballot:

If the La Crosse County Board finds it necessary to increase local spending on roads and bridges due to insufficient state and federal funds, do you support pursuing the enactment of a Premier Resort Area Tax (PRAT) of 0.5 percent as a sales tax on tourism-related goods and services as defined in state law? This option is estimated to raise $6.6 million per year, of which $1.6 million will be shared with the cities, villages and towns for their transportation needs.

Of the four road-funding questions on the referendum, along with the PRAT getting 68.2 percent of the yes votes, also passing with 78% was a county investment of $5 million a year. The PRAT — worded the same way — received 55% of the yes vote in a referendum a year and a half ago.

The two questions that failed were increasing short-term borrowing (73.8% no) and enacting a $56 wheel tax (68.4% no).

5311 – Department stores

5331 – Variety stores

5399 – Miscellaneous general merchandise stores

5441 – Candy, nut and confectionery stores

5451 – Dairy product stores

5461 – Retail bakeries

5499 – Miscellaneous food stores

5541 – Gasoline service stations

5611 – Men’s and boys’ clothing and accessory stores

5621 – Women’s clothing stores

5632 – Women’s accessory and specialty stores

5641 – Children’s and infants’ wear stores

5651 – Family clothing stores

5661 – Shoe stores

5699 – Miscellaneous apparel and accessory stores

5812 – Eating places

5813 – Drinking places

5912 – Drug stores and proprietary stores

5921 – Liquor stores

5941 – Sporting goods stores and bicycle shops

5942 – Bookstores

5943 – Stationery stores

5944 – Jewelry stores

5945 – Hobby, toy, and game shops

5946 – Camera and photographic supply stores

5947 – Gift, novelty and souvenir shops

5948 – Luggage and leather goods stores

5949 – Sewing, needlework, and piece goods stores

5992 – Florists

5993 – Tobacco stores and stands

5994 – News dealers and newsstands

5999 – Miscellaneous retail stores

7011 – Hotels and motels

7032 – Sporting and recreational camps

7033 – Recreational vehicle parks and campsites

7922 – Theatrical producers (except motion picture) and miscellaneous theatrical services

7929 – Bands, orchestras, actors, and other entertainers and entertainment groups

7948 – Racing, including track operation

7991 – Physical fitness facilities

7992 – Public golf courses

7993 – Coin-operated amusement devices

7996 – Amusement parks

7997 – Membership sports and recreation clubs

7999 – Amusement and recreational services, not elsewhere classified